The reality isn’t good, but experts say it isn’t all that bad either

Santa Monica’s real estate market may have peaked recently as local realtors say the combination of high interest rates, taxes, cost of living expenses and general instability are starting to weigh the business.

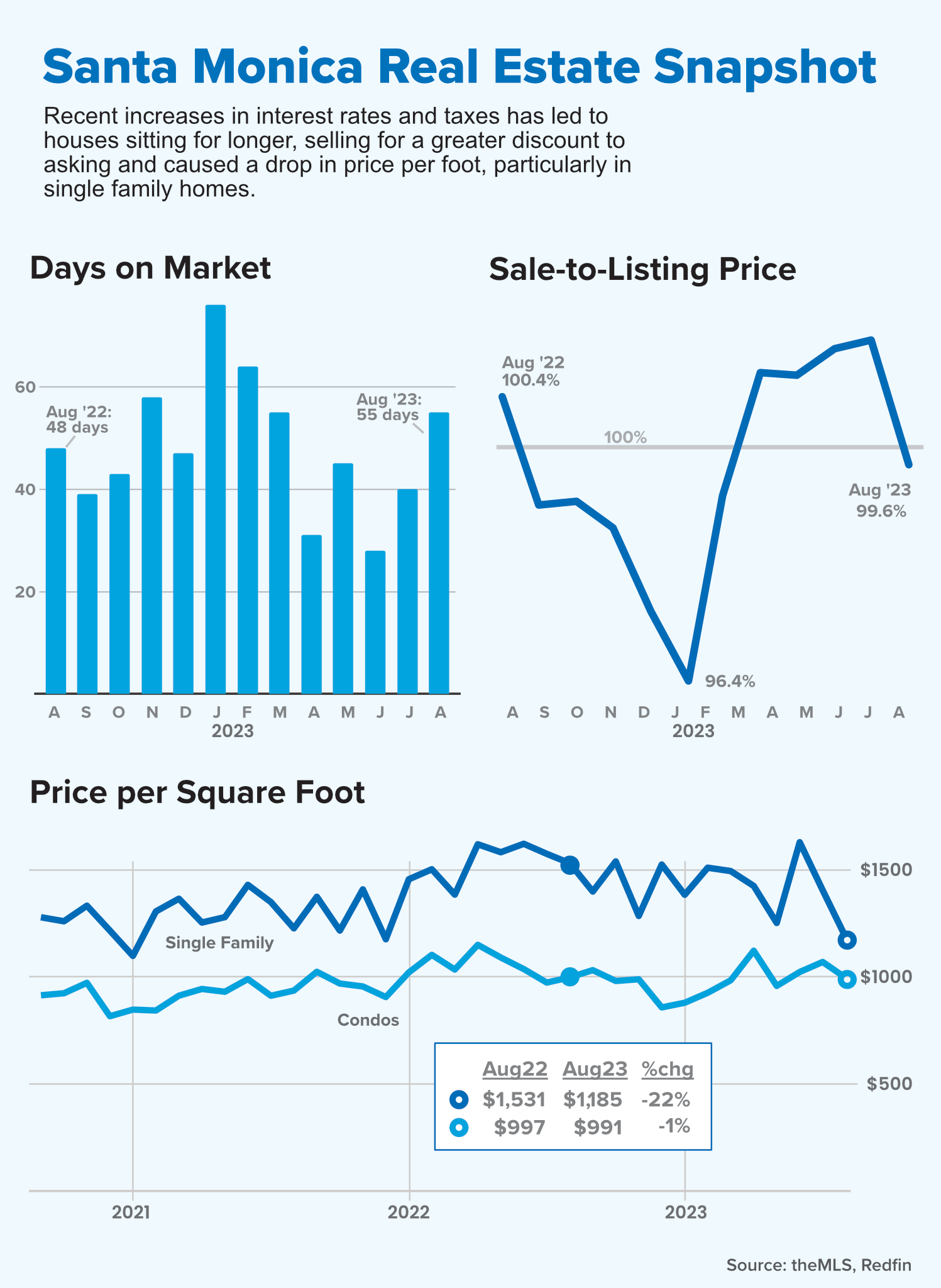

No one is predicting a real estate crash in the city by the sea, but there are early signs of a softening market with an increase in the number of days homes are for sale and fewer homes selling at or above their listed price.

The root of the current market lethargy is a near record interest rate.

In its drive to tame inflation, the Fed has raised its key rate 11 times since March 2022 to about 5.4%, its highest level in 22 years. The rise in long-term rates has contributed to a jump in the average cost of a 30-year mortgage to nearly 8%.

That has driven down home sales everywhere. According to mortgage provider Freddie Mac, the total home sales for July were down 1.2% over the month and 11.8% over the year across the country. Existing home sales continued to decline 2.2% in July and 16.6% as compared to July 2022, according to the National Association of Realtors.

"If you're gonna buy a $1.375 million townhome right now, you're paying close to $9 to $10,000 per month if you include your HOA dues, taxes and insurance. That is huge. Most people typically were in the $5, $5,500 to $6,000 range a handful years ago," said Brian Maser of The Condo Experts.

Realtor Cindy Ambuehl said the rate is strangling supply as much as it is deflecting buyers.

"If I sell my house, I've been there 20 years at 3% interest rate, if I, right now, get a great offer on my house and I want to I sell my house, where am I going to go and get 3% interest rates? So why sell it and have to do that? It just doesn't make sense."

At the state level, a burgeoning insurance crisis has had an impact on home sales.

Since 2022, seven of the top 12 property insurers operating in the state have quit the market entirely or placed restrictions on policy sales due to what they say is an inability to cover the costs of insuring property in high risk areas. State Farm was the most recent player to pull out announcing in May of this year that it would no longer issue new policies in California.

Ambuehl said that has had a real impact on local sales.

"We had people back out of deals because they found out their homeowners insurance was going to be over $200,000 a year. That's not just one house, that's many up in the hills where there have been fires, knock on wood, but they don't even have to be up in the hills for it to be that outrageously expensive," she said.

There have also been L.A. specific factors pinching the market at both ends.

Depressing the high end has been the passage of new taxes on high end home sales. The so-called ‘mansion taxes’ passed in Santa Monica and Los Angeles have prompted sellers to hold onto their properties and see if they can wait out the law rather than take a hit on sale price. At the other end of the spectrum, many locals are struggling just to make ends meet as the result of the ongoing Hollywood strikes and the trickle down from those wage losses pushes homeownership further out of reach for those workers.

Maser said despite the headwinds, the local market isn’t actually bad. It’s just not as good as it was during the recent heyday and that given some time, the markets will adjust.

"What people don't realize is that it's not necessarily a prime situation. Most of those sellers are trying to still get the next level price per square foot. So they're just, they're pushing it and they're sitting and the markets going ‘we're not going to give you that next level value.’ You’ve got to come down to reality but what happens is more inventory sits, that causes properties to kind of slowly get the perception of values falling and then people start chasing them down. So that's usually the beginning of that trend, that's what we're seeing."

Maser said he thought he could sell any property within seven days if it were priced appropriately and sellers who are willing to take regular profit rather than demand record profit are still finding buyers.

Ambuehl said she thought the current malaise would last up to next year’s election when officials eager for reelection would be more motivated to address the interest rate problem. At that point, she said the local market will likely rebound significantly.

"So, what we're very positive about, and we're very optimistic about, is LA," she said. "There is no place like where we live. We're all blessed to live here … And so people still come here, they still want to come here. They'll face these challenges just to be here. We sell this lifestyle. We're not selling a home with four walls. We're selling the lifestyle. We're selling the experience. Get up and go walk on the beach every day and then take a drive up the coast, like where else can you live like this? So I'm very optimistic because we have so much to offer as a lifestyle and a community."

matt@smdp.com